Highly Esteemed & Accomplished

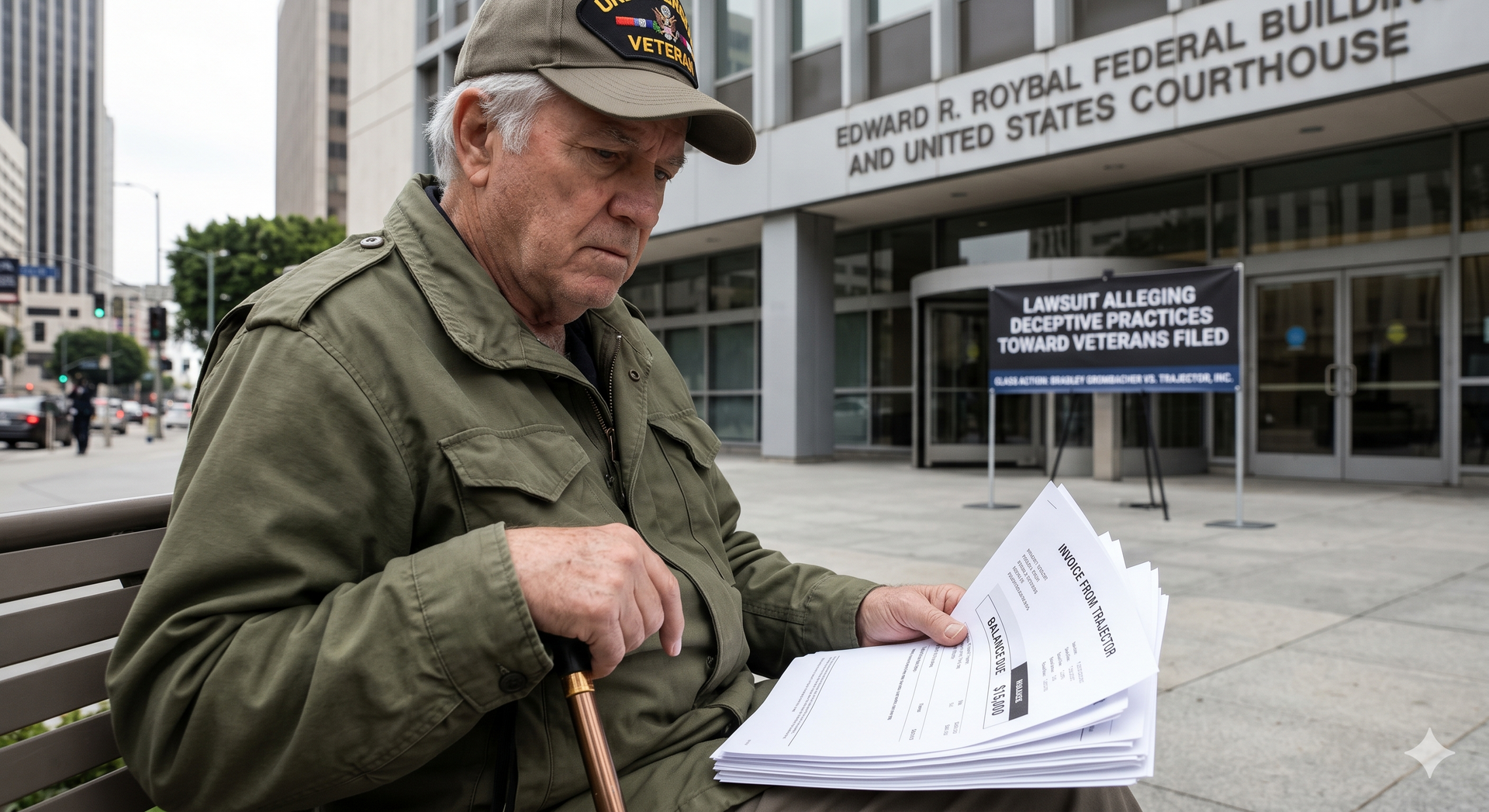

Trajector Faces Class Action Lawsuit Over Alleged Deceptive and Abusive Practices Toward Nation’s Disabled Veterans Los Angeles, CA – April 15, 2026 - Bradley Grombacher filed a nationwide class action lawsuit in Federal court alleging Trajector, Inc. and Trajector Medical, LLC engaged in a widespread scheme to unlawfully charge disabled veterans for assistance with Department of Veterans Affairs (VA) disability claims. According to the complaint, federal law strictly regulates who may assist veterans with preparing, presenting, or prosecuting VA disability claims. Only VA-accredited attorneys, agents, or representatives may provide such services for compensation, and no fees may be charged for assistance with an initial claim. The class action lawsuit alleges that the defendants ignored these requirements entirely, operating without accreditation while charging veterans thousands of dollars, often between $4,500 and $20,000, for services that were either prohibited or required to be free. “Our nation owes its freedom to those brave enough to serve, and Trajector took advantage of these people, violated the law, and continues to prey upon new victims daily,” said attorney Kiley Grombacher of Bradley Grombacher. The complaint further alleges that the defendants’ business model relied on deceptive marketing and misleading contracts that obscured the true nature of their services and fees. Veterans were led to believe they were receiving legitimate assistance designed to maximize their disability ratings. In reality, the plaintiffs claim the Trajector performed tasks that constitute regulated “representation,” including gathering medical records, completing forms, and advising on claim strategy, and all without legal authority. A central component of the alleged scheme involved the use of an automated system known as “CallBot,” which accessed VA systems using veterans’ personal information to monitor changes in their disability benefits. Once a benefit increase was detected, the Trajector issued invoices calculated as a multiple, often five times, of the veteran’s monthly benefit, regardless of whether the company contributed to the outcome. The plaintiffs also allege that the defendants employed aggressive and abusive collection tactics, including repeated phone calls, threats of legal action, and persistent demands for payment, even when the charges were disputed. These practices, the complaint asserts, caused significant financial harm and emotional distress, particularly given the vulnerability of disabled veterans. The case is Gilbert Quijada, Jr. v. Trajector, Inc., USDC Central District of California – Western Division, Case No. 2:26-cv-03792.

Bradley/Grombacher Partner Kiley Grombacher Named to Daily Journal’s 2026 List of Leading Commercial Litigators Westlake Village, California – The Daily Journal named Bradley/Grombacher partner Kiley Grombacher to its 2026 list of Leading Commercial Litigators, recognizing her leadership in high-stakes class actions and mass tort litigation and her work holding corporations accountable in complex consumer, workplace, and product safety cases. Grombacher has built her practice around representing individuals harmed by corporate misconduct, with a focus on nationwide class actions, multidistrict litigation, and cases involving toxic exposure, defective products, and workplace rights. She regularly takes on well-funded defendants in cases that turn on scientific evidence, internal corporate records, and regulatory history. “I’ve always been driven by the simple goal to hold powerful institutions accountable and give people a meaningful path to justice,” Grombacher said. “This recognition reflects the work our team puts in every day to take on complex cases that can create real change.” Among her most notable matters, Grombacher served as lead counsel in nationwide litigation involving Neutrogena aerosol sunscreen products found to contain benzene, a known carcinogen. The case resulted in a class settlement that provided compensation and product vouchers to consumers while drawing national attention to product safety and labeling practices. She also holds a leadership role in ongoing multidistrict litigation challenging the marketing of over-the-counter medications containing phenylephrine. Plaintiffs allege manufacturers promoted the ingredient as an effective nasal decongestant despite longstanding evidence that it is ineffective when taken orally. In addition to consumer cases, Grombacher represents workers in high-impact litigation involving environmental and workplace exposure. She currently advocates for individuals who allege they suffered harm after exposure to hazardous substances, including lead and asbestos, at the Goodfellow Federal Complex in St. Louis. The Daily Journal’s annual list highlights attorneys who lead complex commercial litigation matters across the country, often involving cutting-edge legal theories, extensive evidentiary records, and significant public impact. Grombacher said her work reflects broader shifts across the legal landscape. “We’re seeing increased scrutiny of product safety, corporate transparency, and workplace conditions,” she said. “Litigation plays a critical role in setting standards that protect both consumers and employees.” Grombacher practices out of Bradley/Grombacher’s Westlake Village office and has spent nearly two decades litigating complex cases nationwide. About Bradley/Grombacher Bradley/Grombacher is a plaintiff-side law firm focused on complex litigation, including class actions, mass torts, consumer protection, and employment matters. The firm represents individuals and groups in high-impact cases against corporations and institutions across the country.